Whether it’s higher sticker prices or elevated interest rates, prospective home buyers are feeling the squeeze. The housing market just feels expensive right now.

While there is no denying housing affordability is a challenge for many buyers, zooming out and reviewing key data offers helpful context.

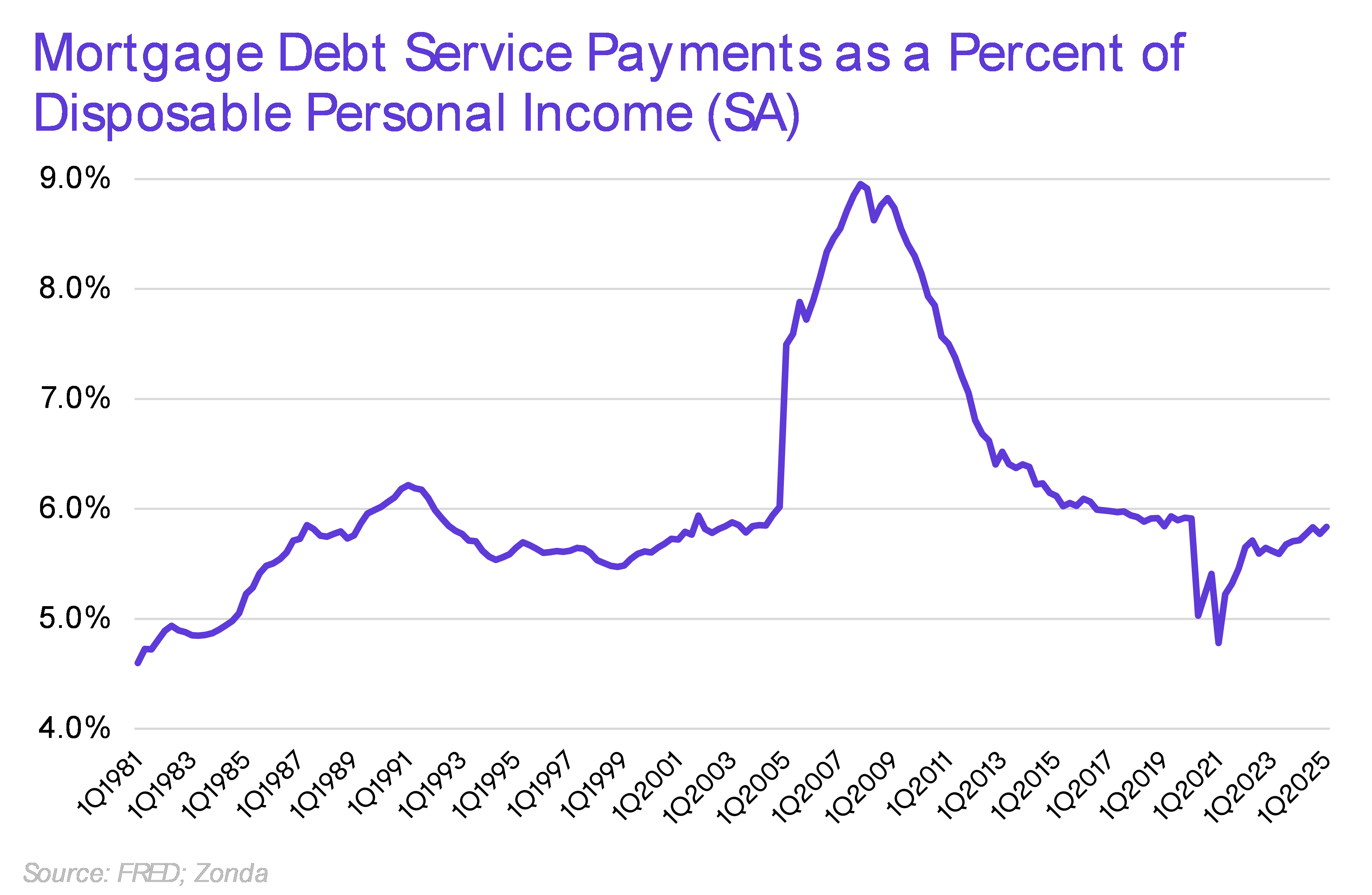

There is more than one way to think about housing affordability. The most common: Looking at home prices and interest rates. Another: Looking at mortgage debt service payments – what people spend to keep up with their mortgages – as a share of disposable income over time. (Disposable income refers to the money households have left to spend or save after paying taxes.)

This comparison offers a clearer picture of housing affordability. It also provides important historical context, comparing the same data during other time periods when economic conditions, taxes, and income levels may have been very different.

Digging Into the Data

Zonda, NewHomeSource’s parent company, analyzed the quarterly ratio of required household mortgage payments to total disposable income using data from the Federal Reserve.

In early 2021, mortgage debt service dropped to just 4.78%.

In the first quarter of 2025, households are spending approximately 5.84% of their disposable income on mortgage payments, a notable jump from the levels seen during the pandemic, but still well below historical peaks.

The chief culprits for the increase since 2021 are home prices and interest rates. The strong housing market combined with rising rates means new buyers are paying more each month. However, the chart reflects an average across all homeowners, including people who locked in ultra-low interest rates before 2022 and are still paying those same rates today. So, while today’s buyers may feel the crunch more than long-time owners, the overall market still looks relatively healthy.

Safe Territory

Even with the affordability challenges facing home buyers, data on mortgage debt service payments suggests most households are not overleveraged. Compare today’s 5.84% to what we saw in 2007, just before the housing crash, when mortgage payments hit a high of 8.95% of income. The current level is much more manageable and suggests that while things are tighter, we are not yet approaching a crisis.

Additionally, another important consideration for prospective home buyers: The affordability challenges keeping home buyers on the sidelines may have ripple effects. With more households opting out of homeownership, there is a larger pool of rental households and this rise in rental demand could have upward pressure on asking rents.

“For those renting, consider that you are at risk every year for your rent to rise,” says NewHomeSource chief economist Ali Wolf. “Buying a home today can be a challenge due to affordability and dissatisfaction with the options out there, but also remember homeownership is one way to lock-in the cost of the largest share of your monthly budget.”